The prop trading landscape in 2026 looks nothing like it did five years ago. There are now hundreds of funded trading programs competing for traders' attention — challenge firms, hybrid models, traditional prop desks, and everything in between. The marketing is sophisticated, the offers are varied, and the gap between a credible program and a fee-collection operation is not always obvious from the outside.

The challenge isn't finding a prop firm. It's knowing how to evaluate one.

Most prop firm comparison content focuses on surface-level details: which firm offers the highest account size, which has the cheapest challenge fee, which has the best profit split percentage. These aren't irrelevant questions. But they're the wrong starting point — because they can all look favorable while the underlying structure of the program works against you.

This article gives you a framework for evaluating any funded trading program across the dimensions that actually matter: capital structure, revenue model, development environment, risk rule design, and long-term fit. Use it before you commit to any program, regardless of how compelling the marketing looks.

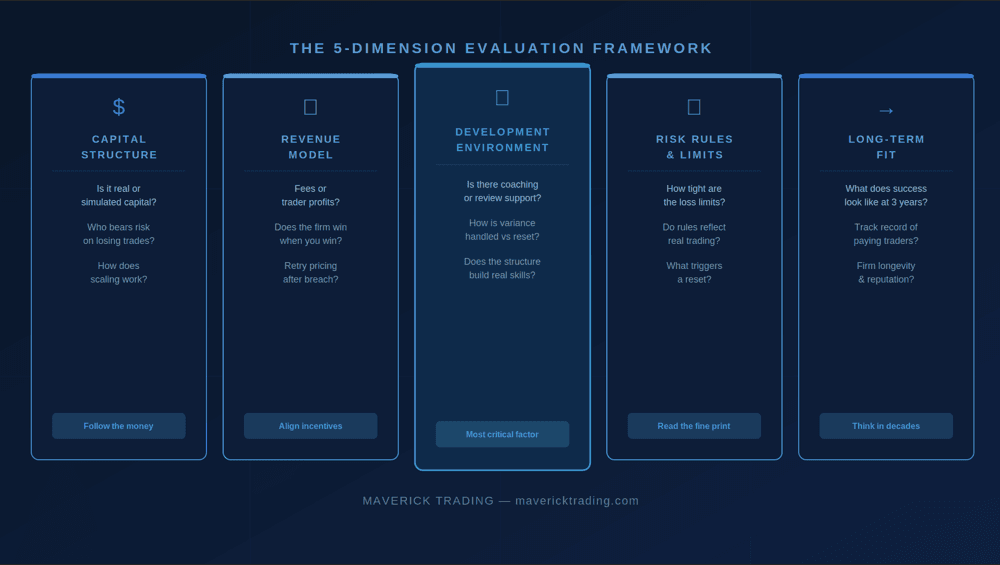

Capital Structure

Is the trading capital real, and who bears the risk when trades go wrong?

Revenue Model

Does the firm earn from your fees — or only when you are profitable?

Development Environment

Does the firm invest in making you a better trader, or just process applications?

Risk Rule Design

Do the rules reflect how real trading works, or are they designed to produce breaches?

Long-Term Fit

What does the relationship look like in year two or three — not just at sign-up?

Dimension 1: Capital Structure — Is the Money Real?

The most fundamental question in any prop firm comparison is one that rarely gets asked directly: is the trading capital real, and who bears the risk when trades go wrong?

In a genuine proprietary trading firm, the firm's own capital is deployed in live markets. When a trader loses, the firm loses real money. That's a meaningful distinction — because it means the firm has a genuine financial stake in selecting and developing traders who can perform. The risk is shared.

In most challenge-based models, the funded account is simulated or paper-traded, particularly at the evaluation stage. Many programs that call themselves "funded" are operating on internal risk models where traders never actually touch live capital — especially until they've proven profitability over multiple periods. The firm's risk exposure is minimal or nonexistent.

Neither model is automatically fraudulent. But they are structurally different, and the distinction affects everything from how you're evaluated to how much the firm cares about your long-term development. When evaluating any program, ask directly: Is the capital deployed in live markets? Does the firm take actual losses when funded traders lose? The answers will tell you a great deal about what you're dealing with.

Dimension 2: Revenue Model — Who Does the Firm Actually Need to Win?

This is the most clarifying question in any prop firm comparison, and it's almost never foregrounded in marketing materials. A firm's revenue model determines whose success it is actually incentivized to support.

There are two primary models:

Earns from your attempts

The firm earns primarily from challenge fees, evaluation fees, and account reset fees. Revenue is generated when traders attempt and fail challenges, retry, and cycle through the evaluation process. The firm is profitable regardless of whether traders ever receive a funded account or generate trading profits.

Earns only when you profit

The firm earns a portion of the trading profits generated by its traders. Revenue only materializes when traders perform. The firm's financial success is directly tied to developing and retaining profitable traders.

The difference in incentive structure is significant. A firm operating on a fee-based model has no financial reason to make the evaluation process easy to pass, provide substantive coaching, or structure risk rules that reflect how professional trading actually works. In fact, the opposite may serve its interests — if tighter rules produce more breaches, that can mean more retry fees.

A firm operating on a profit-share model has every reason to invest in trader development, set reasonable risk parameters, and support traders through the variance that normal trading involves.

The revenue model is the single most revealing signal of whose success a firm is actually built to support.

Dimension 3: Development Environment — Does the Firm Invest in You?

A funded trading program is not just a capital source. At its best, it's a development environment — a structure that helps traders improve their methodology, refine their risk management, and build the consistency that turns a promising trader into a professional one.

The range of what different programs offer here is enormous. Some provide nothing beyond the evaluation rules and a dashboard. Others offer coaching calls, trade review, mentorship from experienced traders, and structured feedback loops. When you're doing a prop firm comparison, this dimension is often the most predictive of whether the relationship will produce meaningful career progress.

Specific things to evaluate:

- Is there access to coaches or mentors with verifiable trading backgrounds?

- How does the firm handle a losing streak — with support and structure, or with a reset and a fee?

- Are there review tools that help traders analyze their own performance over time?

- Does the firm have a track record of traders who have grown their accounts and careers within the program?

The absence of development support doesn't automatically disqualify a program. But it does tell you something important: this is a transaction, not a development relationship. That's worth knowing before you sign up.

Dimension 4: Risk Rules — Do They Reflect Real Trading?

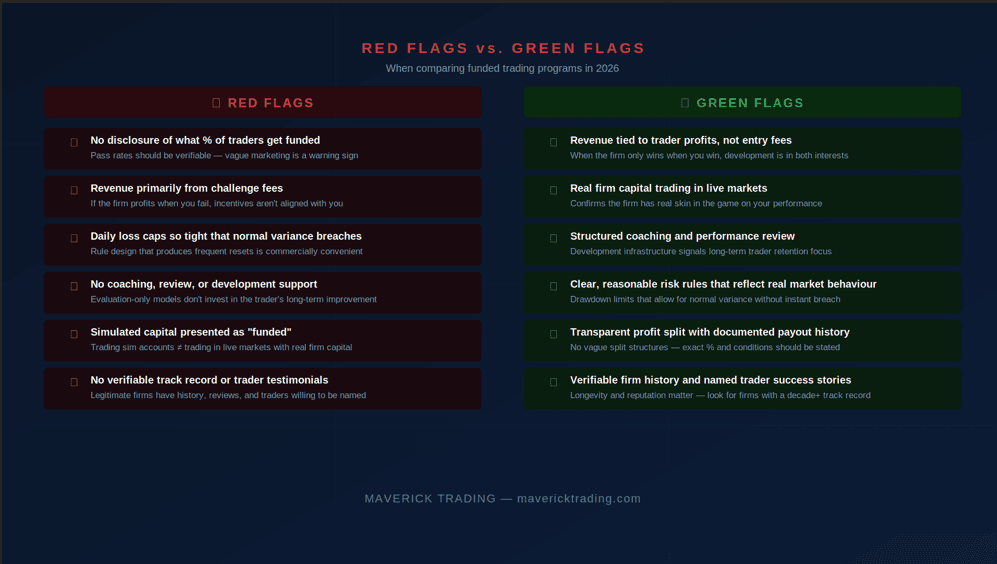

Every funded program has risk rules. The critical question is whether those rules are designed to protect the firm from real losses — or to produce breach events at a commercially useful frequency.

The tell is in the specifics. A daily loss limit of 5% on a $100,000 account means a $5,000 loss in a single session invalidates everything. For many legitimate trading styles, a five-day losing streak where each day loses 1% is perfectly consistent with a sound methodology. But a single bad session can end the evaluation entirely.

When evaluating risk rules, look at:

- Whether the drawdown limits allow for normal multi-day variance without triggering a breach — particularly for swing traders or those who hold positions across sessions

- Whether the rules distinguish between different types of trading (scalping vs. position trading vs. options strategies) or apply blanket limits regardless of style

- What happens when you breach — is there a coaching conversation, a review of what happened, or simply a notification that the account is closed

- Whether the rules are clearly documented upfront or buried in terms and conditions that only become relevant after a breach

Dimension 5: Long-Term Fit — What Does Year Three Look Like?

Most prop firm comparison conversations are focused entirely on getting into a funded account. Far fewer people ask what the program actually looks like two or three years in — if the relationship works as intended.

This is where firm longevity, payout history, and scaling structure become important. A firm that launched eighteen months ago with aggressive marketing and low challenge prices has no demonstrated track record of actually paying traders at scale over time. That's not a disqualifier, but it's a risk factor worth pricing in.

Questions to ask for the long-term view:

- How long has the firm been operating, and can you find verified accounts from traders who have been with the program for multiple years?

- What does the scaling structure look like — can funded account sizes grow as traders demonstrate consistency, and on what terms?

- Is the profit split structure fixed or does it change at different account levels?

- Are there any clauses in the agreement that allow the firm to change payout terms, reduce splits, or close accounts based on factors outside trading performance?

The firms with the longest and cleanest track records in prop trading have been paying traders reliably for years. That consistency is itself a form of due diligence data — and it's one of the most reliable signals available when evaluating a program's credibility.

Firm longevity and verified payout history are among the most reliable signals of program credibility.

How to Use This Framework in Practice

When you sit down to evaluate any funded trading program, the goal isn't to find the firm with the biggest account size or the lowest fee. It's to find the program whose structure, incentives, and development philosophy align with where you are as a trader and where you want to be.

A practical approach: take each of the five dimensions above and ask the firm directly. Not in a forum. Not through marketing materials. Ask the firm — via their support team, in a discovery call, or by reading their contracts and documentation carefully. How a firm responds to direct, specific questions about capital structure, revenue model, and risk rules tells you almost as much as the answers themselves.

Firms that are confident in what they offer will answer these questions clearly. Firms that deflect, use vague language, or redirect to their marketing materials are giving you information — just not the kind they intend to.

The prop trading landscape in 2026 has more options than ever. That's genuinely useful for traders who know how to navigate it. The framework above is designed to help you cut through the volume of options and identify what actually matters: a program built to develop your trading, not to monetize your attempts.

Related Articles

Looking for a Prop Firm That Meets Every Dimension?

Real capital. Profit-based revenue. Structured development. A track record going back to 1997. See how Maverick's approach to trader development compares.

Apply to Maverick Trading →Maverick Trading — Professional Trader Development Since 1997.